CHAPA CALL TO ACTION! Contact Congress to Protect Affordable Housing & Community Development in Tax Reform

Last week, the Senate passed its tax reform plan. The Senate version of the bill retains the Low-Income Housing Tax Credit (LIHTC); tax exemption for private activity bonds, which would preserve the 4% LIHTC; and retains the New Markets Tax Credit and Historic Tax Credit. The next step is for the House and Senate to appoint a conference committee to reconcile the differences between their bills.

Although both the Senate and House tax reform plans will be devastating for so many and threaten the future funding of many programs that serve vulnerable individuals and families, a final tax reform plan is expected to be signed into law by the end of the year. We must act to ensure housing programs are preserved. There are key differences between the House and Senate plans. The Senate version preserves critical programs that produce and preserve affordable housing, including 4% credits, the New Markets Tax Credit, and the Historic Tax Credit.

Call your Representative and Senators now and urge them to protect affordable housing and community development in tax reform. Please ask them to contact House and Senate Leadership and members of the Conference Committee to:

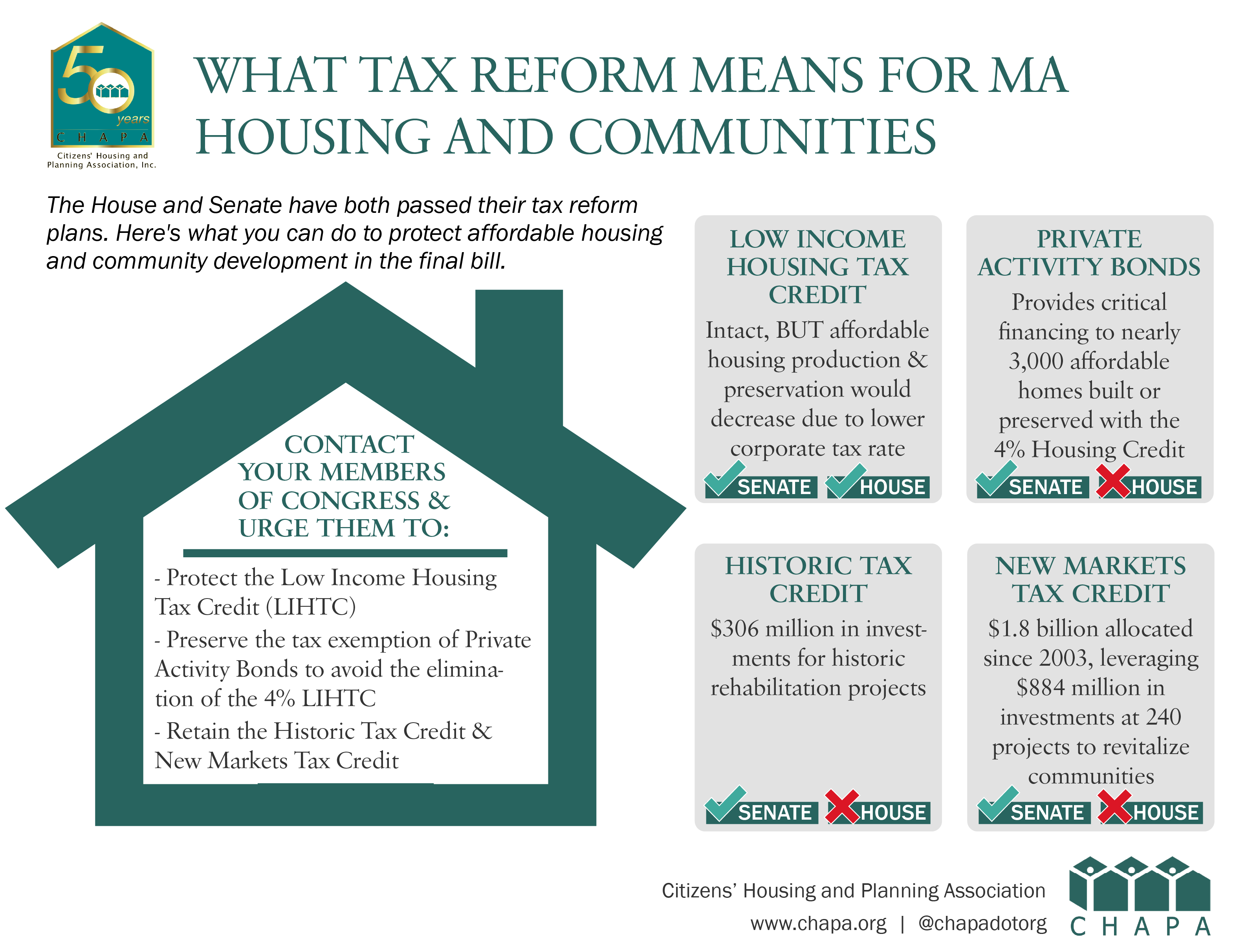

- Protect the Low Income Housing Tax Credit

- Preserve the tax exemption of Private Activity Bonds to avoid the elimination of the 4% Low Income Housing Tax Credit

- Retain the Historic Tax Credit and the New Markets Tax Credit

You can find contact information for your Members of Congress by clicking here.

Description of the Differences between the House and Senate Tax Reform Plans

Low Income Housing Tax Credit

Both the House and Senate version severely devalue LIHTC by lowering the corporate tax rate from 35% to 20%. The Senate plan retains both the 9% and 4% credit. However, the House version eliminates the 4% credit.

If the 4% credit is eliminated, Massachusetts will see nearly a 70% reduction in the number of homes produced or preserved each year by LIHTC. This translates to a loss of over 3,000 homes built or preserved every year.

The Senate version would only reduce LIHTC housing production in Massachusetts by 13%. While this would still mean a projected loss of 8,000 homes over the next decade, this would be less harmful than the House plan.

Private Activity Bonds

As advocates for affordable housing, our top priority for tax reform is to preserve private activity bonds. The House plan eliminates the tax exemption for these bonds, which support the 4% Low Income Housing Tax Credit. These credits account for over half of the homes produced or preserved by LIHTC production.

Historic Tax Credit

The House plan eliminates the Historic Tax Credit while the Senate version retains the credit. The Historic Tax Credit attracts developers to invest in once vacant, deteriorated, and underutilized structures, such as old mills, schools, and hospitals, and transforms them into much needed housing and commercial space. In 2016 alone, this credit supported over $306 million in investments for historic rehabilitation projects.

New Markets Tax Credit

The House tax reform plan eliminates the New Markets Tax Credit while the Senate version keeps this credit. The New Markets Tax Credit is a vital resource for community revitalization efforts in distressed areas. In Massachusetts, it has supported over 240 projects. Since 2003, $1.8 billion in credits have been allocated, which has helped leverage $884.2 million in other investments for these projects.

For updates and more information on the tax reform proposal and its impact on affordable housing, please visit the National Low Income Housing Coalition or the ACTION Campaign.

Help spread the word about what tax reform means for Massachusetts housing and communities!